Calculator App

Plan Your Financial Future with Cash Loans Bear

The Cash Loans Bear Calculator app is a one-stop solution for those who want to borrow money responsibly. By entering basic details, you can estimate monthly payments for different loan types and get practical debt management tips and strategies.

What You Get:

How to Use the Cash Loans Bear Calculator

This tool provides comprehensive loan information and allows you to estimate and compare offers across the following loan types:

To get started, you need to complete these simple steps:

Enter the needed loan details

Enter the following information about your potential loan:

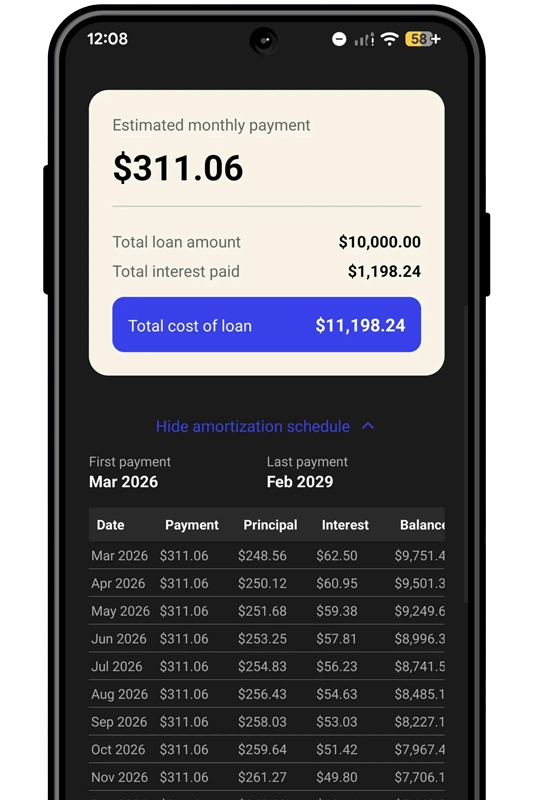

View the final cost

Once you enter the key loan parameters, you will be able to see the total interest paid over the life of the loan. For installment loans, a shorter repayment term results in a lower total cost of borrowing.

Check the amortization schedule

The amortization schedule reveals how your payments are allocated between the loan principal and interest. It also shows due dates and total payment amounts to help you understand how much and when you will need to pay, so you can leave extra room in your budget.

When Does This Calculator Help?

The Cash Loans Bear Calculator helps you crunch the numbers and make an informed borrowing decision. Here’s what you can use it for:

How to Make the Most of This App

Below are several scenarios in which our tool can guide you toward a data-driven decision across various loan types.

Payday Loans

| Loan Amount | Loan Term | Lender’s Fee | Total Cost | What It Means to You |

|---|---|---|---|---|

| $300 | 14 days | $15 per $100 | $345 (APR: 391.07%) | Although the APR is lower on a 30-day payday loan, you can save $15 by choosing the 14-day repayment option |

| $300 | 30 days | $20 per $100 | $360 (APR: 243.33%) |

Personal Loans

| Loan Amount | Loan Term | APR | Monthly Payment | Total Cost | What It Means to You |

|---|---|---|---|---|---|

| $10,000 | 12 months | 8.4% | $871.73 | $10,460.82 | Paying just over $550 per month saves $886.82 overall. A shorter term more than doubles your monthly payment. |

| $10,000 | 36 months | 8.4% | $315.21 | $11,347.64 |

Mortgage

| Loan Amount | Loan Term | APR | Monthly Payment | Total Cost | What It Means to You |

|---|---|---|---|---|---|

| $300,000 | 20 years | 6.2% | $2,184.05 | $524,172.16 | With a 20-year mortgage, you will be debt-free faster and save over $137,000 |

| $300,000 | 30 years | 6.2% | $1,837.41 | $661,466.50 |

Auto Loans

| Loan Amount | Loan Term | APR | Monthly Payment | Total Cost | What It Means to You |

|---|---|---|---|---|---|

| $15,000 | 36 months | 5.3% | $481.69 | $17,340.93 | A 36-month loan saves you just over $900 and helps you own the vehicle sooner. But your monthly payment will increase by $177.55. |

| $16,000 | 60 months | 5.3% | $304.14 | $18,248.63 |

Debt Consolidation Loans

| Balance/Loan Amount | Loan Term | APR | Monthly Payment | Total Cost | What It Means to You |

|---|---|---|---|---|---|

| $5,000 | Full repayment in 59 months | 18.99% | $129 | $19,792.31 | You can save a significant amount by combining your high-interest credit card debts into one loan with a single payment. Savings are higher with a 24-month loan ($5,811 vs. $3,489 for a 60-month loan). A 24-month loan lets you become debt-free twice as fast for a little over $240 per month. |

| $7,500 | Full repayment in 59 months | 21.5% | $212 | $19,792.31 | |

| $12,500 | 24 months | 10.99% | $582.54 | $13,980.96 | |

| $12,500 | 60 months | 10.99% | $271.72 | $16,303.08 |

Early Repayment Scenario

| Loan Amount | Loan Term | APR | Extra Payment | Monthly Payment | Total Cost | Time It Takes to Pay off | What It Means to You |

|---|---|---|---|---|---|---|---|

| $10,000 | 48 months | 7.5% | None | $241.79 | $11,605.87 | 48 months | If you will pay an extra $150 toward your loan, you will pay it off over 28 months and save $677.66 |

| $10,000 | 48 months | 7.5% | $150 | $391.79 | $10,928.21 | 28 months |

Loan Basics Explained

Before you move on to applying for a loan, brush up on the basic terminology.

Loan amount – the amount you actually receive from a lender, usually in one lump sum. It also includes upfront costs, such as origination fees or prepaid interest.

Loan term – the time you have to pay off your loan.

Principal – the original amount you borrowed and agreed to repay.

Interest rate – the base cost of borrowing the principal over a year.

APR – a comprehensive figure that shows the real cost of borrowing over one year. It includes both interest and any associated fees.

Loan payment – typically a fixed amount that consists of both principal and interest that you need to pay in accordance with your repayment schedule.

Due date – the date by which you must make your loan payment.

Pre-approval – a preliminary decision a lender makes after a quick review of your loan application without performing a hard credit check or asking for supporting documents.

Fees – extra charges associated with a loan, for example, for processing your loan request or late payments.

Collateral – a borrower’s asset provided as a security and repayment guarantee to support a loan application.

Default – failing to repay debt according to the agreed-upon terms, typically after multiple missed payments.

Things to Know About Different Loan Types

Making the right borrowing decision may be difficult with so many options available. The table below will help you better understand each loan type and choose the one that is a perfect fit for you:

| Loan Type | Loan Amounts | Repayment Terms | APR | Min. Credit Score Requirements | Collateral | How It Works | Best for |

|---|---|---|---|---|---|---|---|

| Personal Loan | $1,000 – $100,000 | 12–84 months | 5.99% – 35.99% | 620-680, depending on the lender | No | Lump sum deposited to your account and repaid in fixed monthly installments | Large purchases and big life projects |

| Payday Loan | $100 – $1,000 | 7–30 days | 260.71% – 782.14% for a 14-day loan | None | No | Small loan repaid in full by your next paycheck | Small, short-term emergencies and money gaps |

| Mortgage | $100,000 – $1,249,125 (up to 95% of home price) | 3–30 years | 6% – 8% | 620 (500–580 for FHA) | Yes, the house you purchase | Funds go to the seller/escrow; borrower repays monthly over time (rates may be fixed or variable) | Buying a home |

| Auto Loan | $2,500 – $100,000 | 12–96 months | 5% – 29% | 500–600 | Yes, the car you buy | Lender pays dealer/seller; borrower repays with monthly installments | Vehicle purchase |

| Credit Card | $1,000 – $10,000 | Revolving credit | 18% – 30% | 580 | No | Reusable credit line; interest charged only on the used balance | Everyday spending, flexible costs |

What to Pay Attention to Before Taking out a Loan

Each loan is a financial obligation that may affect your overall financial health. Explore these tips to make borrowing responsible and stress-free:

01

Choose the Right Loan Type

Not every loan will be right for your situation. Start by determining the purpose of borrowing, then move to options that meet your needs. For example, payday loans work best for minor unexpected expenses, while personal loans are a good option for large purchases.

02

Compare Offers

Loan conditions vary, even if you search within a specific loan type. Each lender sets their own rules, and even small differences can significantly affect your total loan cost and the overall experience. Pre-qualify with several loan providers and review their terms closely before settling on one offer

03

Read the Terms Carefully

Make sure you fully understand all the loan details, including the APR, term, monthly payments, and due dates. Pay attention to extra fees and the conditions that may cause them. If something is unclear, contact the lender and ask for explanations.

04

Set a Realistic Budget

Before obtaining a loan, take a closer look at your current income and fixed expenses to figure out how much space you have in your budget for an extra monthly payment. Then, calculate your loan payments to make sure they are within your means. The Cash Loans Bear Calculator app will help you do it in just a few taps.

Alternative Ways to Get Money

If borrowing money from a lender does not seem like the best option, consider a few other ways to get extra cash:

Other Features That Make Our App One of a Kind

Taking out a loan is not the only financial decision we make during our lives. At Cash Loans Bear, we want to guide you through every stage of your journey. Here are a few more app features that can be useful in various real-life situations.

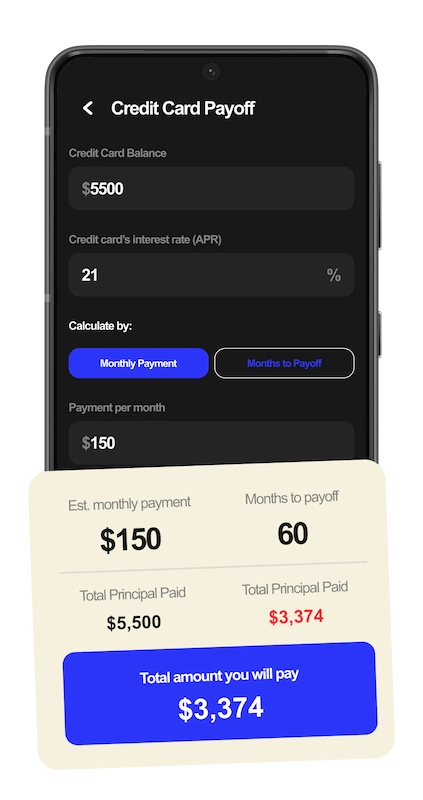

Credit Card Payoff Calculator

This tool is designed to help you repay your credit card balance faster. You can set the number of months within which you plan to pay off your balance and see the amount you need to pay on top of your minimum monthly payment. Alternatively, you can take the amount you’re comfortable paying each month as a starting point and see how fast this extra payment will make you debt-free.

Debt Management Tips and Strategies

With our Debt Payoff Calculator, you can manage multiple debts using proven strategies like the snowball and avalanche methods. Taking into account the chosen strategy, it will provide you with a visual payoff schedule for all loans and credit cards and show you when you will be debt-free and how much you will save.

Investment and Deposit Calculator

If you are going to invest or save money for the future, this calculator will help you estimate how quickly you can reach your financial goal. It requires you to enter an initial deposit amount and your planned monthly contribution to show you how much interest you will earn over a selected period.

A one-stop solution for simple decision-making at your fingertips!

FAQ

How to calculate a payday loan?

Payday loans usually have a fixed fee structure, meaning that a lender charges a set amount for each $100 of the loan. To calculate the total cost of your payday loan, you need to multiply the fee by the amount you borrow, divide the result by 100, and add it to the loan amount. If you want to calculate a payday loan APR, divide the total fees by the amount borrowed, multiply by 365, divide by the loan term in days, and multiply by 100.

How much would a $500 payday loan cost with bad credit?

The exact cost depends on the lender’s fee and the chosen repayment term. If you borrow $500 with a $15 fee per $100, the due amount will be $575. In terms of an APR, such a loan will cost you 391.07% for a common period of 14 days.

How much would a $10,000 personal loan cost per month?

To calculate the exact monthly cost, you need to know your APR and the repayment period. If you obtain a $10,000 loan for 36 months with an APR of 8%, your monthly loan payment will be $313.36. This amount consists of interest and principal. In the first month, you will pay $66.67 toward interest and $246.70 towards principal. Over time, the interest amount will reduce.

How to calculate an interest rate per month on my loan?

A monthly interest rate is determined by dividing your APR converted to a decimal by 12 and then multiplying the result by your current loan balance. When you calculate your loan payments via the Cash Loans Bear Calculator, you can see an amortization schedule that will show you the amount of interest you pay on your loan each month.

Is it a good idea to take out a loan for 60 months or more?

It depends on the loan type, purpose, and your current situation. Large purchases or projects like home improvements may be costly, so a larger loan will require a longer period to pay it back comfortably. However, a longer period always results in a higher total cost. Use our loan calculator to estimate different borrowing scenarios and choose the one with a balanced monthly payment and total interest paid.

How much can I borrow if I can pay $500 per month?

These calculations require you to choose a specific loan type, estimate your APR, and select a repayment period you are comfortable with. For example, if you are going to borrow money for 12 months with an APR of 12%, you can get a personal loan of around $5,600. If the repayment period increases to 24 months, and the interest rate hikes to 13%, the amount rises to nearly $10,500.